What Is ELSS Mutual Fund? A Complete Beginner's Guide to Tax Saving Mutual Funds

Tax season makes most people nervous. You suddenly realize you have not planned your investments, and you start picking random options just to save tax before the deadline. That is a costly mistake.

If you are looking for a smarter way to save tax and grow your wealth at the same time, the ELSS mutual fund is worth understanding properly. It is not complicated. Once you know how it works, it becomes one of the easiest financial decisions you will ever make.

This guide covers everything from scratch, in plain language, so you can start with full clarity.

Start saving tax smarter with expert guidance

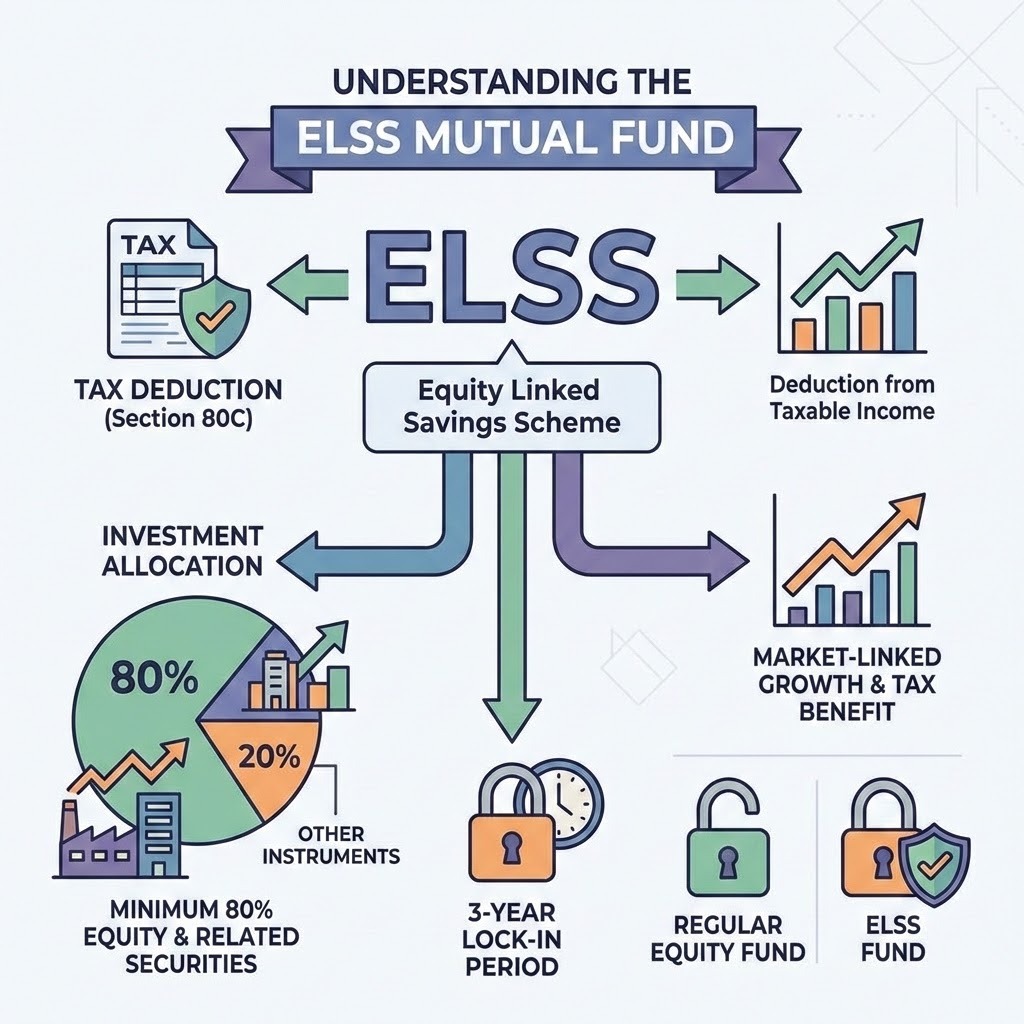

Understanding the ELSS Mutual Fund

ELSS stands for Equity Linked Savings Scheme. An ELSS mutual fund is a category of diversified equity mutual funds that qualifies for tax deduction under Section 80C of the Income Tax Act, 1961.

The fund invests a minimum of 80% of its total corpus in equity and equity-related securities. This means your money goes into shares of companies across different sectors and market caps.

What separates an ELSS mutual fund from a regular equity fund is the mandatory three-year lock-in period and the tax benefit that comes attached to it. You get both market-linked growth and a deduction from your taxable income.

Step by Step Tutorial: How to Invest in Mutual Funds Using Top Mutual Fund Sites

How an ELSS Mutual Fund Actually Works

When you invest in an ELSS mutual fund, your money is pooled with investments from other investors. A professional fund manager uses this pool to buy stocks across large cap, mid cap, and small cap companies based on the fund's investment strategy.

The fund must maintain at least 80% allocation in equities at all times, as mandated by SEBI. The remaining portion can be in debt or money market instruments for stability.

Every rupee you invest is locked in for exactly three years from the date of investment. After the lock-in ends, you are free to redeem, stay invested, or switch. Most investors choose to stay because the compounding just gets better with time.

Key Features of ELSS Tax Saving Mutual Funds

Here is what makes elss tax saving mutual funds genuinely different from other investment options:

Lock-in of only 3 years, the shortest among all Section 80C instruments

Investments can start from as low as Rs 500 per month through SIP

Professionally managed with exposure to equity across market segment

Available in growth option and IDCW (dividend) option

Can be invested as a lump sum or through a systematic investment plan

Returns are market-linked and have historically beaten inflation over long periods

Fully regulated by SEBI, making it a transparent and accountable investment

How a Portfolio Management System Helps Track, Optimize, and Grow Your Investments Efficiently

ELSS vs Other Section 80C Tax Saving Options

Not all tax saving tools are equal. Here is a clear comparison to help you understand where an ELSS mutual fund stands:

The ELSS mutual fund offers the shortest lock-in, the highest return potential, and a reasonably light tax structure at maturity. That combination is hard to beat.

Who Should Consider Investing in ELSS?

Elss tax saving mutual funds are not for everyone equally. Here is a simple profile of who benefits most:

Salaried individuals in the 20% or 30% income tax bracket

Self-employed professionals who want tax savings with growth potential

Young investors starting their first tax-saving investment

Anyone with a financial goal that is at least 3 to 5 years away

Investors who are comfortable with short-term market fluctuations

People who want to begin equity investing with a disciplined approach

If you tick even three of these boxes, an ELSS mutual fund is likely a smart fit for you.

Step by Step Guide to Start Investing in ELSS Mutual Funds

Starting your investment in elss tax saving mutual funds is easier than most people think. Follow these steps:

Complete your KYC using PAN card, Aadhaar, and a passport-size photo

Choose a trusted investment platform, either directly through an AMC or via a registered distributor

Compare ELSS mutual fund options based on 3-year and 5-year returns and fund manager track record

Decide whether you want to invest as a lump sum or start a monthly SIP

Choose between growth option and IDCW option based on your preference

Submit your application and make the payment online

Save the investment confirmation as proof for your 80C deduction claim

Private Equity Investment in India 2026: Trends, Sectors, and Opportunities Investors Should Watch

Tax Benefits Explained in Simple Terms

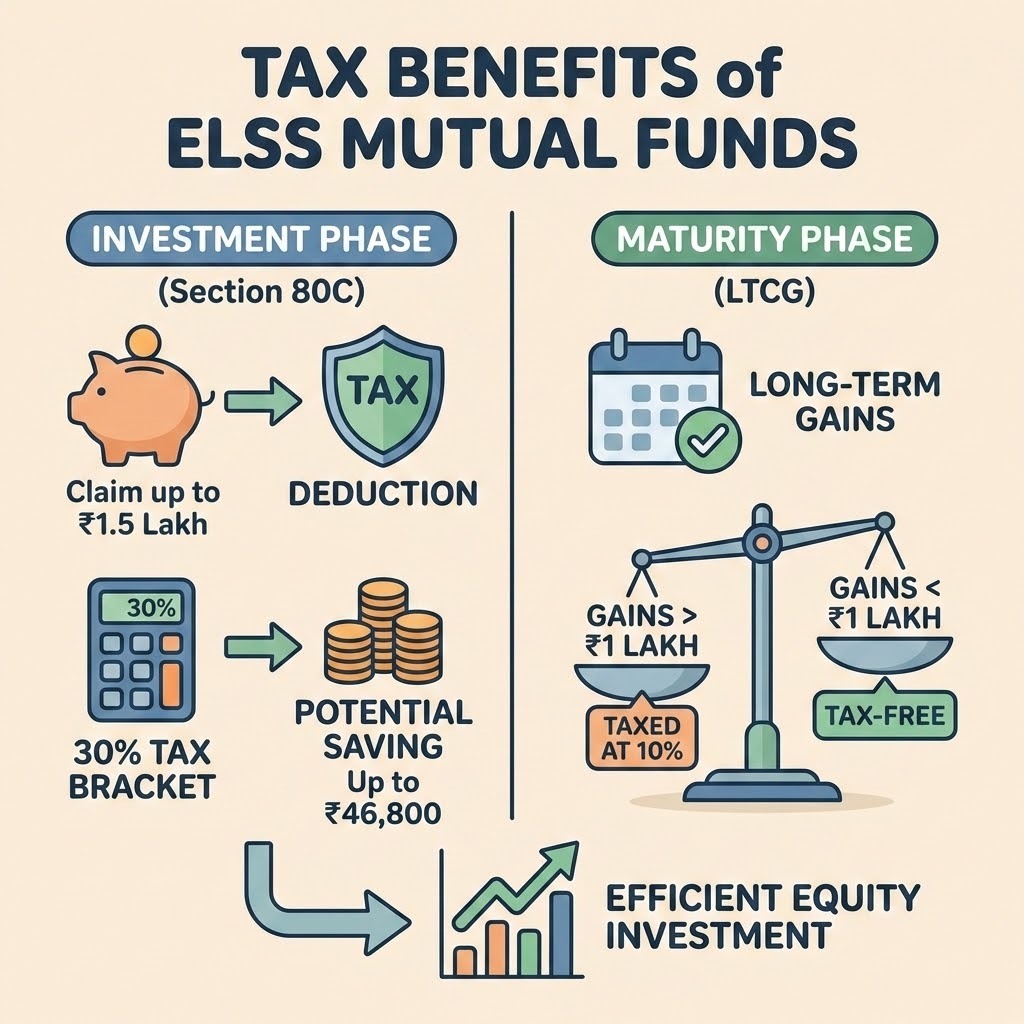

The primary reason most people invest in elss tax saving mutual funds is Section 80C. You can claim a deduction of up to Rs 1.5 lakh per financial year under this section.

If you are in the 30% tax bracket, that means a direct tax saving of up to Rs 46,800 per year including cess. No other equity investment gives you this benefit.

At maturity, your gains are classified as long-term capital gains. Only the gains exceeding Rs 1 lakh in a financial year are taxed at 10%. Gains below that threshold are completely tax-free. This makes the ELSS mutual fund one of the most tax-efficient equity investments available.

Common Mistakes Investors Make with ELSS

Many investors waste the potential of their ELSS mutual fund by repeating these errors:

Investing only in January or February in a panic, instead of spreading investment across the year

Choosing a fund based solely on recent one-year performance rather than consistent long-term returns

Redeeming immediately after the 3-year lock-in without considering the growth trajectory

Investing in too many ELSS schemes at once, which creates unnecessary overlap

Treating it purely as a tax tool rather than a long-term wealth building instrument

Types of Life Insurance Policies in India

Smart Tips to Get the Best from Your ELSS Mutual Fund

Follow these practical tips to genuinely benefit from your investment:

Start SIP in April itself, at the beginning of the financial year

Do not pause or stop SIP during market falls, those are the best months to accumulate units

Review your ELSS mutual fund performance once a year, not every month

Hold beyond the mandatory 3 years to allow compounding to deliver meaningful results

Stick to one or two well-rated schemes rather than spreading thin across many funds

Unlisted Shares Investment Explained for First Time Investors

Why ELSS Stands Out Among Tax Saving Instruments

Among all Section 80C options, elss tax saving mutual funds offer a unique combination that others cannot match. You get the shortest lock-in, the potential for the highest returns, and a structure that builds long-term wealth while reducing your current tax liability.

The transparency of mutual fund investing, the SEBI regulation, and the flexibility of SIP all add to its appeal. For a generation that wants money to work harder and smarter, the ELSS mutual fund is a natural starting point.

Conclusion

Tax saving should never be a last-minute decision made in panic. When you understand your options clearly, you make better choices. An ELSS mutual fund gives you equity growth, a short lock-in, and real tax relief under one roof.

Start early in the financial year, invest through SIP, and give your money the time it needs to grow. Elss tax saving mutual funds are not just about saving tax today. They are about building wealth for tomorrow. The best time to start was yesterday. The next best time is right now.

Contact us for expert tax-saving advice

10 Frequently Asked Questions

1. What does ELSS stand for in mutual funds?

ELSS stands for Equity Linked Savings Scheme. It is a type of mutual fund that invests primarily in equities and offers tax deduction under Section 80C.

2. What is the lock-in period for an ELSS mutual fund?

The mandatory lock-in period is 3 years from the date of each investment. This is the shortest lock-in among all Section 80C tax saving instruments.

3. Can I invest in ELSS through SIP?

Yes. SIP is a highly recommended way to invest in elss tax saving mutual funds. Each monthly installment has its own separate 3-year lock-in calculated individually.

4. What is the maximum tax benefit from ELSS investment?

You can claim up to Rs 1.5 lakh deduction under Section 80C. In the 30% tax bracket, this saves up to Rs 46,800 per year including cess.

5. Are ELSS returns completely tax-free?

No. Long-term capital gains above Rs 1 lakh per year are taxed at 10%. Gains up to Rs 1 lakh annually are tax-free.

6. Is ELSS safe for first-time investors?

It carries market risk since it is equity-based. However, the disciplined lock-in and SIP approach make elss tax saving mutual funds suitable for beginners with a long-term mindset.

7. Can I withdraw ELSS investment before 3 years?

No. Premature withdrawal is not allowed. Every unit must complete its individual 3-year lock-in before redemption is possible.

8. How many ELSS funds should I invest in?

One or two well-performing ELSS mutual fund schemes are sufficient. Too many funds create portfolio overlap and dilute the focus of your investment.

9. Can NRIs invest in ELSS mutual funds?

Yes, NRIs can invest in elss tax saving mutual funds subject to FEMA compliance and KYC requirements. Some fund houses may have specific restrictions for NRIs.

10. What happens to my investment after the 3-year lock-in ends?

Your units become freely redeemable. You can withdraw fully, partially, or remain invested. There is no obligation to exit, and many investors choose to stay invested for continued growth.

Powered by Froala Editor

-Meaning,-Benefits,-Risks-&-Smart-Investment-Strategy_11zon.png)

.png)