What Are MTF Interest Rates? Meaning & Complete Cost Breakdown

Introduction

If you have ever used a Margin Trading Facility (MTF) or are considering it, one of the most important things to understand is the MTF interest rate, the cost you pay for borrowing funds from your broker to trade.

In this guide, we break down what MTF interest rates mean, how they are calculated, what they typically cost, and how they affect your overall returns. Whether you are a seasoned investor or just getting started with leveraged trading, this blog will help you make an informed decision.

How a Portfolio Management System Helps Track, Optimize, and Grow Your Investments Efficiently

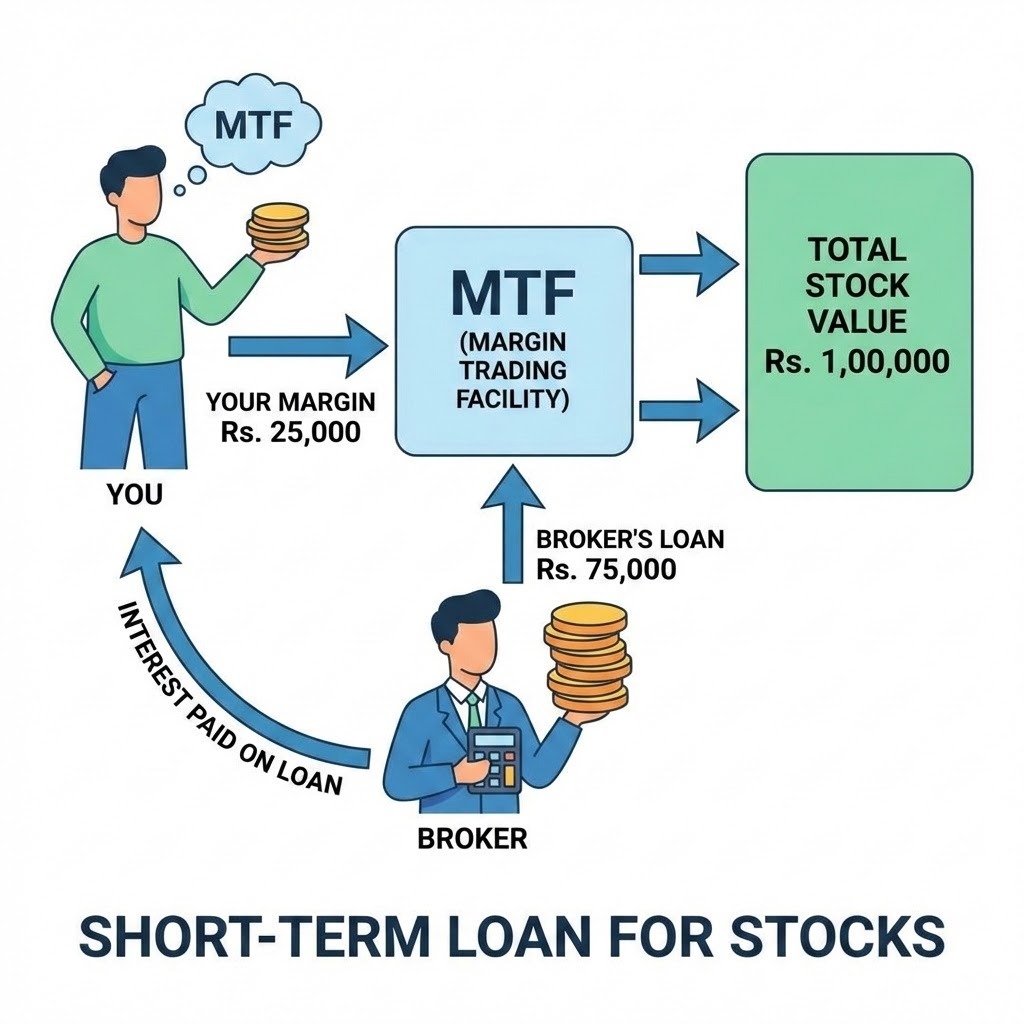

What is MTF (Margin Trading Facility)?

MTF, or Margin Trading Facility, is a SEBI and exchange-approved product that allows you to buy stocks by paying only a portion of the total trade value upfront. Your broker funds the remaining amount, and you pay interest on that funded portion until you close or square off your position.

Think of MTF as a short-term loan from your broker, specifically designed for stock market trading.

Quick Example: You want to buy shares worth Rs.1,00,000. You have Rs.25,000 in your account. Using MTF, your broker funds the remaining Rs.75,000. You pay interest only on the Rs.75,000 funded amount, not on your own Rs.25,000.

Types of Life Insurance Policies in India

What Are MTF Interest Rates?

MTF interest rates are the charges your broker levies on the funded amount, the money they lend you for your trade. This rate is expressed as an annual percentage (p.a.) but is applied daily.

In India, MTF interest rates typically range between 9.65% p.a. to 18.25% p.a., depending on:

Your broker and their pricing plan

The size of your funded position

Prevailing market interest rates and the broker's own borrowing costs

Duration of holding the position

Rates are indicative. Always verify with your broker before trading.

Unlisted Shares Investment Explained for First Time Investors

How is MTF Interest Calculated?

MTF interest is calculated on a daily basis using the following formula:

Daily Interest = (Funded Amount x Annual Rate) / 365 Total Interest = Daily Interest x Number of Days Position is Held

Worked Example

You buy shares worth Rs.4,00,000 using MTF. You pay Rs.1,00,000 from your own funds. Your broker funds the remaining Rs.3,00,000 at 14.6% p.a. (0.04% per day).

This is why MTF is best suited for short to medium-term trades, not long-term investing.

Complete Cost Breakdown: What You Actually Pay in MTF

MTF is not just about interest. There are several other charges involved that add to your total cost:

All these charges combined can meaningfully eat into your trading profits. It is crucial to factor in the complete cost, not just the headline interest rate, before entering an MTF position.

Categories of Portfolio Management in India: A Complete Classification Guide

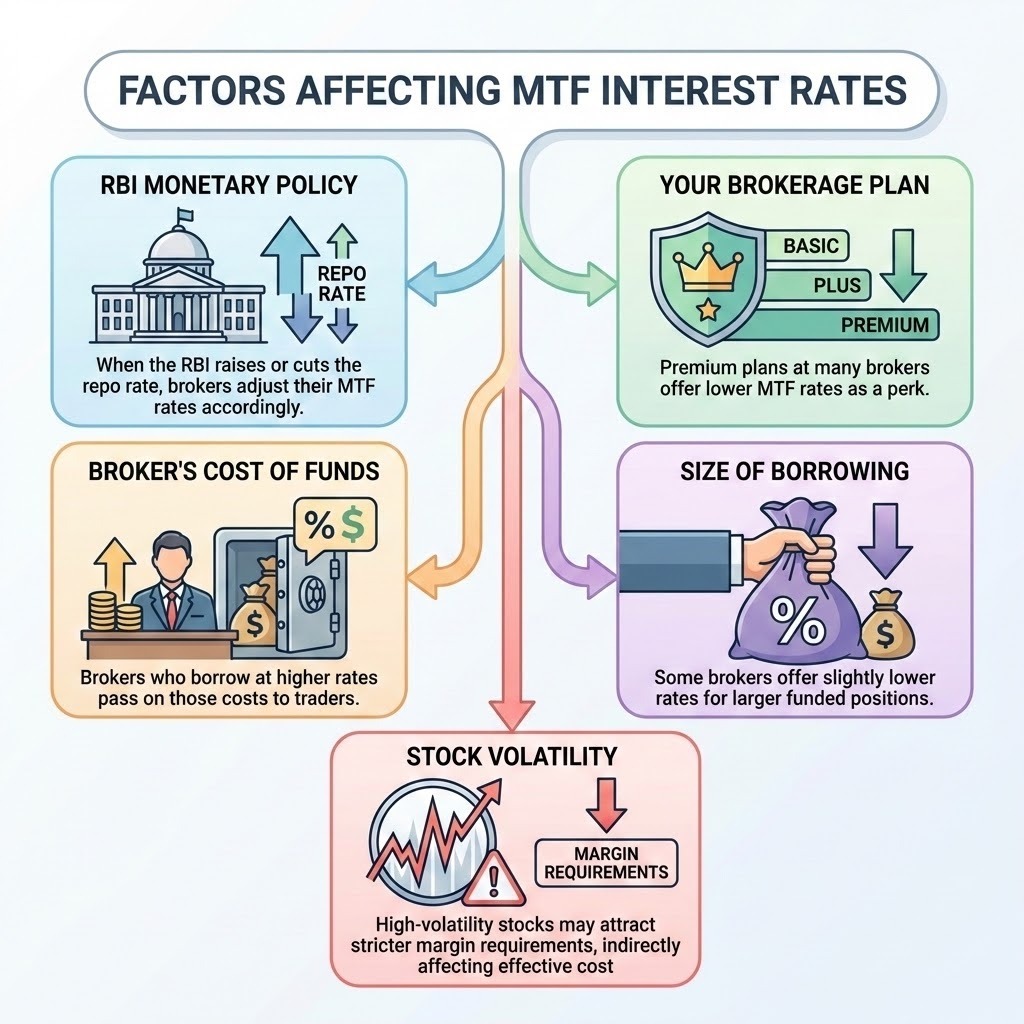

Factors That Affect MTF Interest Rates

MTF interest rates are not fixed forever. They can change based on several factors:

RBI Monetary Policy: When the RBI raises or cuts the repo rate, brokers adjust their MTF rates accordingly.

Broker's Cost of Funds: Brokers who borrow at higher rates pass on those costs to traders.

Your Brokerage Plan: Premium plans at many brokers offer lower MTF rates as a perk.

Size of Borrowing: Some brokers offer slightly lower rates for larger funded positions.

Stock Volatility: High-volatility stocks may attract stricter margin requirements, indirectly affecting effective cost.

How MTF Interest Impacts Your Returns

This is the part most traders overlook. Let us see how MTF interest affects your net profit.

Scenario Analysis

Stock Price: Rs.100 | Shares Bought: 1,000 | Total Value: Rs.1,00,000 | Your Margin: Rs.25,000 | Broker Funded: Rs.75,000 @ 14.6% p.a.

If price rises to Rs.110 in 10 days:

Gross Profit: Rs.10,000

MTF Interest (10 days): Rs.300

Net Profit: Rs.9,700

If price falls to Rs.90 in 10 days:

Gross Loss: Rs.10,000

MTF Interest (10 days): Rs.300

Total Loss: Rs.10,300

When the trade goes against you, you bear the market loss and pay interest on top of it. This is the double risk of MTF.

Categories of Mutual Funds in India: A Complete Classification Guide

When Should You Use MTF?

MTF works well in specific situations:

Best Situations to Use MTF

You have strong conviction in a short-term price movement

The trade duration is short, days to a few weeks, not months

Expected returns significantly exceed the interest cost

You are an experienced investor who can monitor positions daily

You have emergency funds to handle margin calls if needed

When to Avoid MTF

Long-term investing, as interest compounds and erodes wealth over time

Highly volatile stocks, since sudden price drops can trigger forced selling

When you cannot monitor your positions actively

Beginners with limited market experience

Tips to Manage MTF Interest Costs

Compare brokers before using MTF, as rates can vary by 5% to 8% between brokers

Opt for premium brokerage plans if you trade frequently on margin

Keep holding periods short, as interest accumulates every single day

Always set a stop-loss to limit downside before entering an MTF trade

Calculate your breakeven return to ensure the trade makes sense after interest

Monitor your margin levels daily to avoid forced square-offs

Private Equity Investment in India 2026: Trends, Sectors, and Opportunities Investors Should Watch

Conclusion

MTF can be a powerful tool when used wisely. It amplifies your buying power and allows you to capture short-term market opportunities without liquidating your existing holdings. However, the interest rate is a real and daily cost that directly reduces your net returns.

Before using MTF, always calculate the complete cost, understand the risks of leverage, and ensure your expected returns comfortably exceed the borrowing cost. As always, investing with knowledge is the first step to investing well.

At FinBerg, we help our clients make informed and disciplined investment decisions, from equity and mutual funds to portfolio management and wealth planning. Reach out to us to know more about how to grow your wealth strategically.

Disclaimer

This blog is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any securities. MTF involves significant risk, leverage can amplify both gains and losses, and you may lose more than your initial investment. All rates and charges mentioned are indicative and subject to change, please verify with your broker before trading. FinBerg Private Wealth is an AMFI Registered Mutual Fund Distributor and SEBI Registered Sub-Broker. For personalized advice, consult a SEBI Registered Investment Adviser.

Powered by Froala Editor