How Much Life Insurance Coverage Do You Really Need in 2026?

Introduction

Life insurance is really important for my familys future. The cost of living and healthcare is going up in 2026 so it is very important to choose the life insurance. Many people buy life insurance. They have a hard time figuring out how much coverage they need to protect their family.

If I have little life insurance coverage my family will be in a tough spot financially. On the hand if I have too much life insurance coverage I will be paying too much money for premiums.

I need to understand how life insurance coverage I really need so my family can have financial security and I can have peace of mind. Life insurance is key, to making sure my family is okay so I need to get the life insurance coverage right.

Protect your family’s future with the right life insurance plan

Understanding Life Insurance Coverage

1. What Is Life Insurance Coverage?

Life insurance coverage refers to the financial protection provided by a life insurance policy. If the insured person passes away during the policy term, the designated beneficiaries receive a death benefit that can help cover expenses and maintain financial stability.

The purpose of life insurance coverage is to replace lost income, settle debts, fund future expenses, and support dependents financially.

2. Why Choosing the Right Insurance Coverage Amount Matters

Selecting the correct insurance coverage amount is critical because it determines the level of protection your family will receive.

A suitable insurance coverage amount can help:

Replace lost income

Pay off outstanding debts

Fund children's education

Cover daily living expenses

Protect long-term financial goals

3. Common Misconceptions About Life Insurance

Many people make assumptions that can leave them underinsured.

Common misconceptions include:

Employer-provided insurance is enough

Young professionals do not need coverage

Coverage requirements never change

More coverage is always better

Understanding your actual life insurance coverage needs helps avoid these mistakes.

Term Insurance Myths Busted: 10 Things Most Indians Still Believe

Why Life Insurance Needs Are Changing in 2026

1. Rising Cost of Living

Inflation continues to impact household expenses, making adequate life insurance coverage more important than ever.

Families face increasing costs related to:

Housing

Utilities

Food

Transportation

Childcare

These expenses should be considered when calculating an appropriate insurance coverage amount.

2. Higher Education Costs

Educational expenses continue to rise globally.

Parents often use life insurance coverage to ensure that children can continue their education even if an unexpected event occurs.

3. Increasing Healthcare Expenses

Healthcare costs are becoming a significant financial burden for many families.

A sufficient insurance coverage amount can help protect dependents from financial stress associated with medical expenses.

4. Growing Financial Responsibilities

Modern households often carry multiple financial obligations, including:

Home loans

Personal loans

Credit card debt

Vehicle loans

These liabilities should be included when determining your life insurance coverage requirements.

5. Changing Family Structures

Family responsibilities vary significantly depending on marital status, number of dependents, and aging parents.

Your life insurance coverage should reflect these unique circumstances.

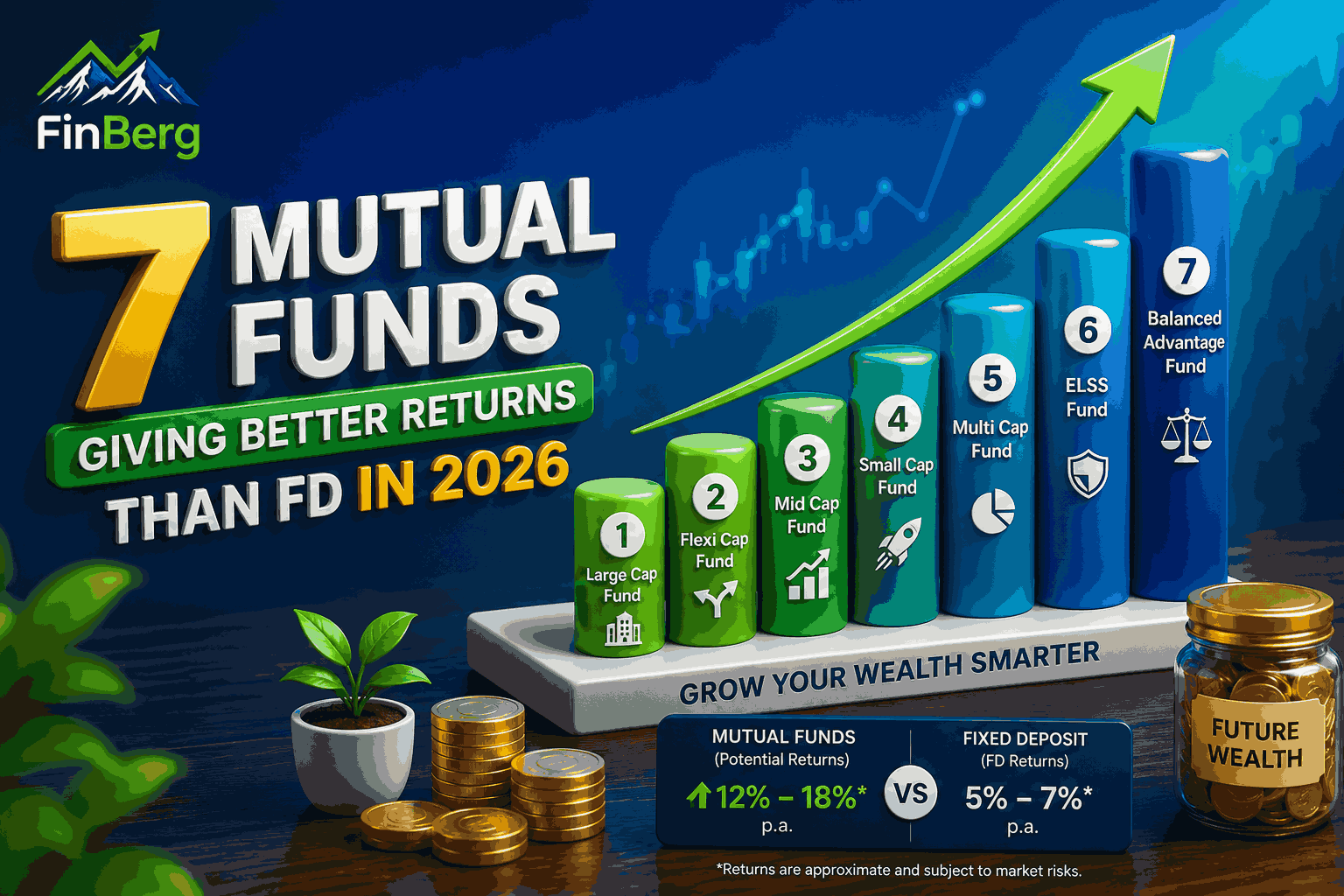

₹500 SIP Can Make You a Crorepati: Best Funds to Start Today

Factors That Determine How Much Life Insurance Coverage You Need

1. Your Annual Income

One of the most common approaches is income replacement.

Financial experts often recommend life insurance coverage equal to 10–15 times annual income.

This helps maintain your family's lifestyle and financial stability.

2. Outstanding Debts

Your insurance coverage amount should be sufficient to eliminate major debts.

Examples include:

Mortgage loans

Personal loans

Business loans

Credit card balances

Paying off debts prevents financial burdens from being passed to family members.

3. Family Living Expenses

Daily living expenses should be carefully evaluated.

Consider:

Rent or mortgage payments

Utility bills

Food expenses

Transportation costs

Healthcare expenses

These factors significantly influence the required insurance coverage amount.

4. Children's Education Goals

Education planning is a major reason families purchase life insurance coverage.

Future expenses may include:

School tuition

College fees

International education costs

Professional training programs

5. Future Financial Goals

Your life insurance coverage should support long-term objectives such as:

Retirement planning

Wealth preservation

Family financial security

Legacy planning

6. Existing Assets and Investments

Before finalizing your insurance coverage amount, consider:

Savings accounts

Fixed deposits

Mutual funds

Existing insurance policies

Investment portfolios

These assets may reduce the amount of additional coverage required.

Unlisted Shares Price List & Companies in India 2026

Popular Methods to Calculate Life Insurance Coverage

1. Income Replacement Method

This method suggests multiplying annual income by 10–15 years.

For example:

Annual Income: $80,000

Coverage Needed: $800,000–$1.2 million

This approach provides a simple estimate of required life insurance coverage.

2. Human Life Value (HLV) Method

The HLV method evaluates future earning potential and financial contribution.

It often provides a more accurate insurance coverage amount because it considers long-term income projections.

3. DIME Method

The DIME method calculates:

Debt

Outstanding liabilities that need repayment.

Income

Future income replacement requirements.

Mortgage

Housing-related financial obligations.

Education

Future education funding needs.

This method provides a comprehensive estimate of life insurance coverage requirements.

4. Expense-Based Method

This approach focuses on projected future expenses rather than income replacement alone.

Many financial advisors use this method to determine an appropriate insurance coverage amount.

What Is Overnight Trading? Benefits, Risks, and Who Should Consider It

How to Calculate Your Insurance Coverage Amount in 2026

1. Calculate Annual Family Expenses

Determine yearly household costs.

2. Add Outstanding Debts

Include all current liabilities.

3. Estimate Future Education Costs

Account for inflation-adjusted education expenses.

4. Include Future Financial Goals

Consider retirement and wealth preservation objectives.

5. Subtract Existing Assets

Deduct savings and investments available to beneficiaries.

6. Determine Final Insurance Coverage Amount

The remaining figure represents the estimated insurance coverage amount needed for financial security.

Example Scenarios for Life Insurance Coverage

1. Young Professional (Age 25–35)

Characteristics:

Growing income

Limited liabilities

Long earning horizon

Recommended life insurance coverage:

10–12 times annual income.

2. Married Individual With Children

Characteristics:

Dependents

Education planning needs

Mortgage obligations

Recommended insurance coverage amount:

15–20 times annual income.

3. Business Owner

Characteristics:

Business liabilities

Employees

Family responsibilities

Recommended life insurance coverage:

Based on business obligations and income replacement needs.

4. Pre-Retirement Individual

Characteristics:

Reduced liabilities

Established investments

Wealth preservation goals

Recommended insurance coverage amount:

Based on remaining obligations and estate planning objectives.

These PMS Strategies Delivered Massive Returns in 5 Years

How Much Life Insurance Coverage Do Different Families Need?

Common Mistakes When Choosing Life Insurance Coverage

1. Choosing Coverage Based Only on Premium Cost

Lower premiums may result in insufficient protection.

2. Ignoring Inflation

Future expenses will likely be higher than current expenses.

3. Underestimating Future Financial Needs

Many individuals underestimate long-term family requirements.

4. Not Reviewing Coverage Regularly

Your life insurance coverage should evolve as your circumstances change.

5. Depending Solely on Employer Insurance

Employer policies often provide limited protection.

6. Ignoring Debt Obligations

Outstanding liabilities can significantly impact family finances.

Exchange Traded Funds (ETF): Meaning, Benefits, Risks & Smart Investment Strategy

Life Insurance Coverage vs Insurance Coverage Amount

Signs You May Need More Life Insurance Coverage in 2026

1. Marriage

New responsibilities often increase coverage needs.

2. Birth of a Child

Children create long-term financial obligations.

3. Purchasing a Home

Mortgage commitments require additional protection.

4. Starting a Business

Business owners may need greater financial security.

5. Increased Income

Higher income often means larger replacement requirements.

6. Taking on New Debt

Additional liabilities may require a higher insurance coverage amount.

Benefits of Having the Right Insurance Coverage Amount

1. Financial Security for Dependents

2. Debt Protection

3. Education Funding

4. Wealth Preservation

5. Peace of Mind

6. Long-Term Financial Stability

The right insurance coverage amount ensures that loved ones remain financially protected even during difficult circumstances.

Why Mutual Funds Are Popular in India: Benefits, Risks and Long Term Potential

Best Practices for Reviewing Life Insurance Coverage

1. Review Policies Annually

2. Recalculate After Major Life Events

3. Account for Inflation

4. Reassess Financial Goals

5. Consult Financial Professionals

6. Compare Available Policy Options

Regular reviews help ensure your life insurance coverage remains aligned with changing needs.

7 Mutual Funds Giving Better Returns Than FD in 2026

Conclusion

Figuring out the right life insurance is a deal. You need to think about how money you make what you owe, who depends on you what you want for your kids education and what you already have.

When you look at all these things and check your policy from time to time you can be sure your family will be okay if something happens to you. Getting the right life insurance now means life insurance will take care of your loved ones and give you life insurance security and confidence, about money for years to come.

Secure your financial future with Finberg. Explore our insurance solutions and take the first step toward protecting your loved ones with confidence. Visit Finberg today to get started.

FAQs

How much life insurance coverage do I need in 2026?

The right life insurance coverage depends on your income, debts, family responsibilities, future goals, and existing assets.

What is the best way to calculate an insurance coverage amount?

Popular methods include the Income Replacement Method, Human Life Value (HLV) Method, and DIME Method, which consider income, debts, mortgage, and education expenses.

Is 10 times my annual income enough life insurance coverage?

It can be a good starting point, but families with children, large debts, or long-term financial goals may require higher coverage.

How often should I review my life insurance policy?

You should review your policy at least once a year or after major life events such as marriage, childbirth, or purchasing a home.

Does life insurance coverage need to increase with inflation?

Yes. Inflation can significantly increase future living expenses, education costs, and healthcare expenses, making periodic policy reviews important.

What factors affect the insurance coverage amount I need?

Key factors include income, outstanding debts, family size, children's education plans, lifestyle expenses, and future financial goals.

Should stay-at-home parents have life insurance coverage?

Yes. Stay-at-home parents provide valuable services such as childcare and household management that would be costly to replace.

Can I have multiple life insurance policies?

Yes. Many individuals combine multiple policies to achieve adequate financial protection and flexibility.

What happens if my life insurance coverage is too low?

Insufficient coverage may leave your family struggling to manage expenses, debts, and future financial commitments.

How do I know if I need additional coverage?

You may need more coverage after major life changes such as marriage, having children, buying a house, starting a business, or taking on additional debt.

Powered by Froala Editor