Difference Between SIP and Mutual Fund Explained: A Complete Guide for New Investors

Investing can feel confusing for beginners. Two terms that often create confusion are mutual funds and SIP. This guide explains the mutual fund vs SIP difference in a clear, step-by-step way so new investors can start with confidence. It also explains how SIP works in mutual fund investments and which approach suits different financial goals in 2025.

The goal is simple. After reading this guide, you will understand the mutual fund vs SIP difference, know how SIP works in mutual fund schemes, and be able to decide whether to start an SIP, invest a lump sum, or combine both methods for better outcomes.

SIP vs Mutual Fund Know Where to Start Your Investment Journey

What is a Mutual Fund

A mutual fund is an investment product that pools money from many investors. Professional fund managers buy stocks, bonds, or other securities according to the fund’s objective.

A mutual fund can be equity oriented, debt oriented, hybrid, index linked, sector specific, or tax saving. When discussing mutual fund vs SIP difference, remember that mutual fund refers to the product and SIP refers to the method of investing into that product.

Key features of a mutual fund

Professional management by fund managers.

Diversification across many securities to reduce single-stock risk.

Different categories for different goals.

Easy liquidity through buying and selling at Net Asset Value.

Read More: Comparing the Best PMS Companies in India: Performance, Fees, and Services Explained

What is SIP

A SIP or Systematic Investment Plan, is a method of investing a fixed amount regularly into a mutual fund. SIPs help investors build discipline and benefit from rupee cost averaging over time.

Understanding how SIP works in mutual fund investments is important for every beginner. SIP automates the investment process and reduces the stress of market timing.

How SIP works in mutual fund step by step

Choose a mutual fund scheme that matches your goal.

Fix the amount to invest each period.

Select the frequency for the SIP.

Authorize automatic debit from your bank.

Units are allotted at the NAV on the investment date.

Over time rupee cost averaging helps buy more units when NAV is low.

Compounding grows the investment value over long horizons.

Learn More: Equity Fund Investment vs. Mutual Fund: Which Is Better for 2025?

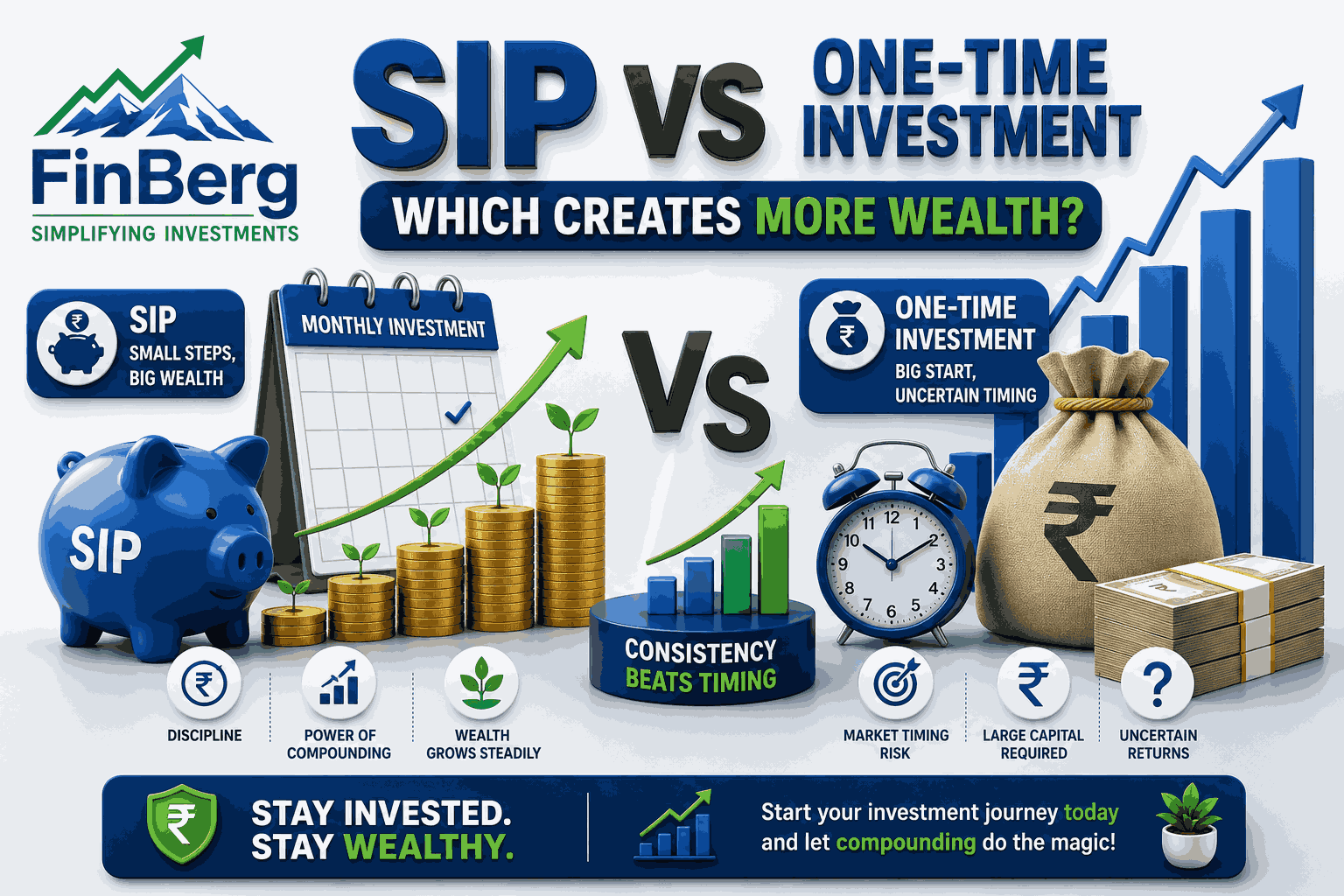

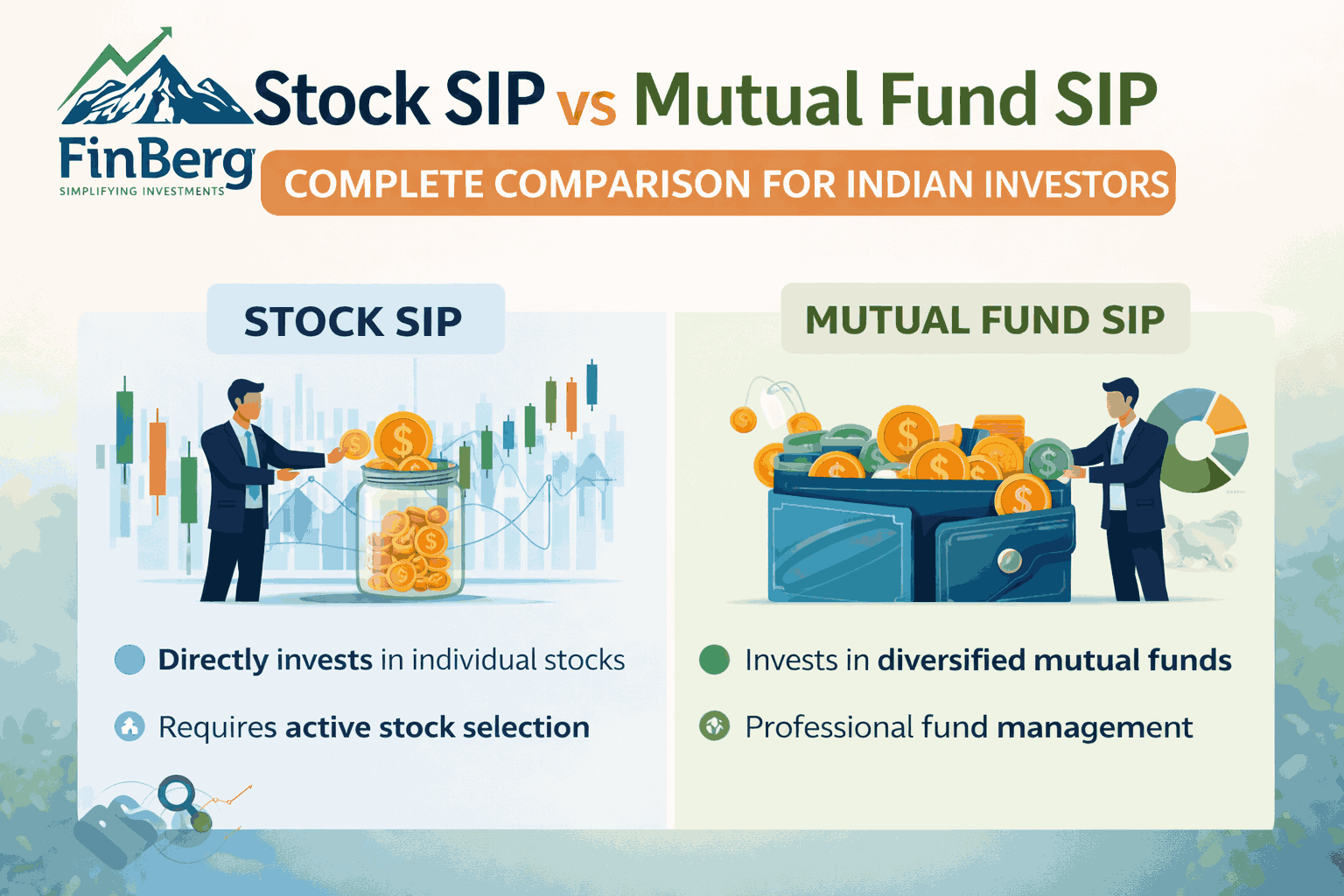

Core mutual fund vs SIP difference

The simplest way to see the mutual fund vs SIP difference is this. Mutual fund is the vehicle. SIP is one of the ways to invest in that vehicle. Both are not mutually exclusive. You can invest in a mutual fund through an SIP or via lump sum purchases.

Comparison points to highlight the mutual fund vs SIP difference

Definition: A mutual fund is a portfolio product; SIP is a periodic investment method.

Timing: A mutual fund lump sum requires market timing; SIP reduces timing risk.

Amount: mutual funds accept lump sum or SIP amounts; SIP suits small monthly budgets.

Suitability: mutual fund lumps suit investors with spare capital; SIP suits salaried or disciplined investors.

Risk management: SIP reduces volatility through averaging.

Why SIP matters: how SIP works in mutual fund for new investors

If you are new, the best way to start is to understand how SIP works in mutual fund schemes practically. SIP encourages small regular contributions that compound over years. It eliminates the need to pick the best entry point and makes investing habitual.

Practical example of how SIP works in mutual fund

Invest 2,000 rupees monthly into an equity mutual fund for 10 years.

Each month you buy units at that month’s NAV.

When NAV falls, you receive more units.

When NAV rises, you receive fewer units.

Over time your average cost becomes smoother.

Compounding grows the total value if the fund shows positive long-term returns.

Read More: How a Life Insurance Advisor Can Help You Secure Your Family’s Future in 2025

Mutual fund vs SIP difference in returns and risk

A key investor question is whether SIP returns beat lump-sum returns. The answer depends on market conditions and investor time horizon. If the market is in a long bull run, a lump sum invested at the right time can yield higher returns. However, predicting market tops and bottoms is extremely hard. SIP reduces the guesswork by spreading investments.

Risk and return factors

Lump-sum mutual fund investments show higher return variability.

SIP reduces the impact of volatility through cost averaging.

Both methods are subject to market risk because the underlying assets are the same.

The mutual fund vs SIP difference is not about product quality but about investment discipline and timing.

Types of mutual funds you can use with SIP

You can start an SIP in almost any mutual fund category. Choosing the correct category depends on the investor’s objective, time horizon, and risk appetite.

Equity mutual funds for long-term growth.

Large-cap or multi-cap funds for moderate risk.

Mid-cap and small-cap funds for aggressive growth.

Hybrid funds for balanced exposure.

Debt funds for capital preservation.

ELSS funds for tax-saving with a lock-in period.

Knowing how SIP works in mutual funds for each category helps you plan contributions appropriately.

How to decide between SIP and lump sum: a step-by-step process

Clarify your financial goal and timeline.

Identify your risk tolerance level.

If you have a large surplus and strong market conviction, consider lump sum in phases.

If you prefer discipline and lower timing risk, start SIPs for the long term.

Consider a combination: invest part as a lump sum and the rest as SIP.

Review performance annually and rebalance according to goals.

Applying this process addresses the mutual fund vs SIP difference in a practical way.

Learn More: Why You Need a Health Insurance Advisor in 2025: Smart Planning for Rising Medical Costs

Example comparison table: mutual fund vs SIP difference at a glance

The table clearly highlights the mutual fund vs SIP difference for quick reference.

Benefits of using SIP explained

Helps new investors start small and stay consistent.

Encourages financial discipline through automated investing.

Smooths out the average cost you pay for units.

Enables compounding over long horizons.

Reduces emotional reactions to market noise.

Learning how SIP works in mutual fund investments helps you see why SIP is often recommended for first-time investors.

Read More: What Happens to Unlisted Shares After an IPO in 2025? A Complete Investor Guide

Mistakes to avoid when using SIP or mutual funds

Stopping SIPs during market falls. Consistency matters more during volatile times.

Selecting funds based only on past returns. Look at the process and fund manager.

Ignoring fund costs like expense ratio and exit load.

Choosing funds misaligned with time horizon and risk appetite.

Failing to periodically review the portfolio and rebalance.

Avoid these errors to better understand the mutual fund vs SIP difference and improve investing outcomes.

Choosing the right mutual fund for SIP: checklist

Check fund objective and how it matches your goals.

Review 3-year and 5-year rolling returns rather than short-term spikes.

Verify fund manager experience and fund house credibility.

Look at expense ratio for long-term cost impact.

Confirm fund consistency and downside protection.

Use how SIP works in mutual fund logic to simulate monthly units purchased.

This checklist helps you pick funds suitable for SIP strategy.

Read More: Best Financial Advisor in India [2025]

Tax implications and how SIP works in mutual fund taxation

Tax treatment depends on whether funds are equity or debt oriented. SIP installments are treated as individual investments for capital gains calculation.

Equity mutual funds: Long-term capital gains above threshold taxed at specified rate if held beyond one year.

Debt mutual funds: Different holding period rules apply for long-term and short-term taxation.

ELSS funds offer tax benefits with a lock-in period.

Understanding how SIP works in mutual fund taxation helps you plan withdrawals and reduce tax burden legally.

Advanced use cases combining SIP and mutual fund strategies

Start SIP in multiple categories to create a balanced asset allocation.

Use SIP for recurring contributions and top up with a lump sum when the market dips.

Switch allocation gradually over time from equity to debt as retirement approaches.

Use goal-based SIPs for education, house down payment, and retirement separately.

These strategies show how SIP complements mutual fund investing and clarify the mutual fund vs SIP difference for different life stages.

Learn More: Best Stock Advisory Firm in India [2025]

Performance tracking and rebalancing: practical steps

Track NAV and corpus growth monthly or quarterly.

Review fund performance against benchmark and category peers.

Rebalance yearly to maintain target asset allocation.

Switch funds only after careful review, not emotional reactions.

Use portfolio analytics to see how SIPs and lump sums jointly perform.

Understanding how SIP works in mutual fund practice is crucial for disciplined performance tracking.

How to start a SIP: simple action plan

Complete KYC online to meet regulatory requirements.

Choose the mutual fund and the scheme for SIP.

Set the amount and frequency.

Link bank mandates for auto debit.

Monitor first three transactions to validate setup.

Keep records for taxation and review.

This step by step plan shows exactly how SIP works in mutual fund practice for beginners.

Common myths about mutual fund vs SIP difference

Myth: SIP guarantees returns. Reality: SIP reduces risk but does not guarantee returns.

Myth: SIPs are only for small investors. Reality: High net worth individuals use SIPs to average positions.

Myth: Lump sum is always better. Reality: Lump sum needs correct timing which is very hard to achieve.

Myth: SIPs are complicated. Reality: Modern platforms make setup easy and transparent.

Debunking these myths clarifies the mutual fund vs SIP difference.

Example scenarios: when to use SIP and when to choose lump sum

You received a bonus and want to invest slowly: start a SIP and invest a portion as a lump sum.

You have a long horizon, like 15 years for retirement: prioritize SIP for consistent compounding.

You plan a short-term purchase in two years: prefer debt funds or liquid mutual funds rather than equity SIP.

You are new to investing: begin with SIP to build habit and experience.

These scenarios illustrate the practical application of the mutual fund vs SIP difference.

Conclusion

The mutual fund vs SIP difference is a question of method versus product. A mutual fund offers professionally managed portfolios, while SIP provides an effective, disciplined method of investing into that portfolio. For new investors, understanding how SIP works in mutual fund systems helps remove confusion and sets the stage for long-term wealth creation.

Start with clear goals, choose appropriate mutual funds, and use SIPs to build discipline and take advantage of rupee cost averaging. Combine periodic reviews, smart rebalancing, and occasional lump-sum investments to create a powerful, goal-oriented portfolio in 2025 and beyond.

Learn How SIPs and Mutual Funds Work, Simplified for New Investors

FAQs

What is the main mutual fund vs SIP difference?

Mutual fund is the product, and SIP is a method of investing into that product. SIP spreads risk, while a lump sum exposes you to immediate market timing.How does SIP work in a mutual fund when markets fall?

When markets fall, SIP buys more units at lower NAVs, aiding rupee cost averaging and improving average purchase cost.Can I stop SIP anytime?

Yes, you can stop SIPs, but stopping during market downturns can cost you lost compounding benefits that come with time.Are SIPs safe for new investors?

SIPs reduce timing risk and help build habit, but they remain subject to market risk depending on the fund category chosen.How do I calculate returns from SIP?

Returns are usually annualized based on XIRR formula. Many fund platforms provide SIP return calculators to estimate future corpus.Does SIP work only in equity mutual funds?

No SIPs are available across equity, debt, hybrid and tax saving funds. Understanding how SIP works in mutual fund categories is important.What is the minimum SIP amount?

Most funds allow SIPs from small amounts such as 500 rupees monthly. This makes investing accessible.How often should I review my SIP investments?

Review quarterly to track performance and rebalance annually or when goals change.Is a lump sum better when markets are low?

Lump sum can be better if you have conviction about market valuation and sufficient capital. Generally, combining lump sum and SIP is safer.How does taxation differ with SIP?

Each SIP installment is a separate purchase and taxed based on the holding period and asset type for capital gains calculations.

Powered by Froala Editor